US Stocks Distended on Fed’s Wall of Money. US Citizens Disquieted by Wall of Worry

The US economy faces tremendous turmoil: a pandemic proliferating a virus for which there is no vaccine, an apparently fathomless global recession, prodigious levels of unemployment, spiralling national debt, central bank debt monetisation masquerading as stimulus, a controversial and capricious presidential election, escalating trade and diplomatic tensions with China and deeply divisive domestic social and racial enmities.

Judging by the price action of US stock indices, these tumultuous conditions represent a mere bagatelle.

The S&P has staged a precipitous 44% rally since the market crash in March, erasing the entirety of its earlier losses, while the Nasdaq, which includes tech-giants Apple and Facebook, as well as relative newcomers like Zoom has posted a new all-time high.

The widening divergence between Wall Street and Main Street has developed into a chasm, as stock markets have detached from fundamentals, their pricing no longer driven by bleak economic data and elevated geopolitical risk, but the accelerated expansion of the Federal Reserve balance sheet, creating virtual reality stock prices.

An occurrence exacerbated by the influx of amateur day traders, drawn to the allegedly one-way-bet of long positioning. Citi strategists cite this development as a key reason their Panic/Euphoria Model recently recorded its highest reading for stock market euphoria since 2002, raising the odds of a correction in the next year to over 70% by their metric.

Given the overbought technical picture and breach of a three month uptrend, the correction may materialise sooner than many blinkered bulls might wish.

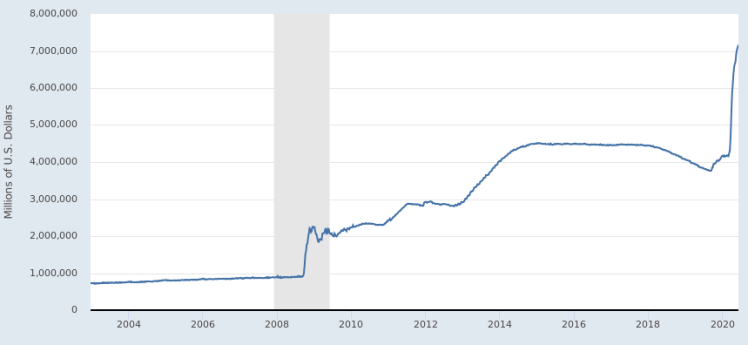

Once firmly held attitudes around moral hazard have now been consigned to the file for inconvenient truths, in favour of determinedly limitless bailouts. In support of this cause, the Fed balance sheet has increased by a staggering $4.5 trillion in the last month, the total now exceeding $7.5 trillion.

Former New York Fed President William Dudley, believes the Fed balance sheet could reach $10 trillion before the conclusion of this cycle of intervention, a scale equivalent to 50% of the US economy.

US Treasury Secretary Steven T. Mnuchin announced a relief package passed by Congress amounting to $2.3 trillion, using the Fed as a conduit for the funds. This programme is of a different magnitude to the previously unparalleled TARP intervention, originally authorising expenditures of a then record $700 billion in 2008, later reduced to $475 billion by the Dodd-Frank Act.

US National Debt now exceeds $26 trillion ($26,000,000,000,000), which equates to 130% of GDP. At the beginning of 2020, the government was already running an annual deficit of $1 trillion. Since March, owing in large part to the coronavirus mitigation package, the US has been accumulating additional debt at a rate of $1 trillion a month. https://www.usdebtclock.org/

Quantitative Easing (the electronic creation of money with which a central bank undertakes asset purchases of longer-term securities via open market operations, in order to increase the money supply, reduce interest rates across the curve and theoretically encourage lending and investment) the once radical, unconventional monetary policy tool, has become the de rigueur response in the era of zero (or negative) interest rates.

The Fed doesn’t expect to raise its benchmark interest rate until 2023, a stance made crystalline by Chairman Jerome Powell; ‘we’re not even thinking about thinking about raising rates‘, taking central bank forward guidance into hitherto unknown realms of commitment.

The Fed has also announced it will end the steady tapering of its asset purchases, instead continuing to buy US Treasurys and mortgage-backed securities, ‘at least at the current pace‘.

There had been concerns in financial markets these purchases, which the Fed claims are supporting market functioning, might end as they have been tapered in recent weeks. Under current arrangements the Fed will buy $20 billion in Treasurys a week and up to $22.5 billion in mortgage bonds.

The spectrum of debt the Fed is willing to purchase in pursuit of ‘price stability‘ now knows few bounds, encompassing corporate debt, Mortgage Backed Securities, Municipal Bonds, Exchange Traded Funds and even Junk bonds.

Having engineered an equities rally into price territory representative of expansive economic growth, the Fed faces a quandary: how to continually sate the market appetite it has unleashed? The currently popular maxims among investors ‘follow the Fed and don’t fight the Fed’ can only really be satisfied by ever more inventive monetary policy.

Thus the fevered speculation among some economists that the central bank will adopt the recondite and controversial policy of yield curve control: a manoeuvre which targets theoretically unlimited Quantitative Easing at specific bonds across the tenor spectrum, in the pursuance of perpetual interest rate suppression.

Such a previously unconscionable intervention would dispel the last vestiges of belief in the principal of a free market economy. The peremptory banishment of Adam Smith and the invisible hand to market equilibrium.

Perhaps the greatest, self imposed challenge for the Federal Reserve in the longer term, is how do they reduce, cease or even reverse interventions of such gargantuan proportions without causing critical market strain? Weaning a market so utterly reliant on central bank stimulus may prove as problematic as the economic contraction the measures were introduced to counteract. Dishearteningly, the Fed have already failed to unwind previous stimulus several times in the last decade.

A disturbing example of this phenomena occurred in 2013, when bond markets became hysterical after the Fed signalled its intention to begin unwinding a prevailing programme, triggering a surge in bond yields sardonically known as the ‘taper tantrum‘. Last year, the Fed elected to abandon the nascent reversal of its bond purchases over concern it was creating market tensions.

Here then is the manifestation of that now banal term, the new normal. A market place rendered disfunctional without repeated hits of central bank intervention. Its ability to provide accurate insight into the economic cycle obliterated. Hooked on a spiral of monetary stimulant.

If the economic recovery, as appears likely, is a protracted and arduous process, a period where ever enlarged central bank balance sheets must eventually meet reach their vanishing point, investor cold turkey will be execrable. Caveat Emptor.

Stephen Cherry. 11th June 2020.