Andy Haldane, Bank of England Chief Economist has spoken publicly in the aftermath of the Bank’s latest despondent forecast, in which it predicts the deepest economic contraction in 300 years (-25%) and a sharp rise in the unemployment rate toward 9% (the highest since 1994). Mr Haldane says he fears the impact of the pandemic could be more significant than the Bank’s already pessimistic prognostications, owing to what he describes as “dread-risk”: a self reinforcing negative feedback loop made manifest by apprehensive households and businesses simultaneously disengaging from economic activity, leading to a perpetual deterioration.

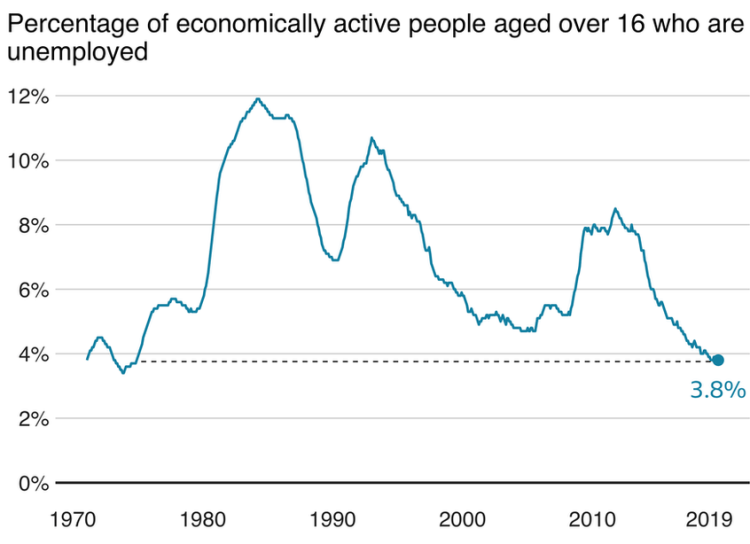

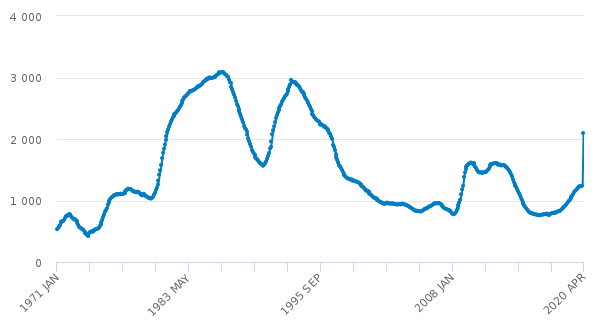

UK unemployment has been low in recent years, mirroring figures from the early 1970’s (+/- 4%). However, anecdotal evidence has suggested many households are already facing the impact of a sharp rise in unemployment. In his comments, Mr Haldane expressed trepidation about a deterioration toward levels last seen in the 1980’s recession, when the jobless rate exceeded 12%. These anxieties have proven efficacious, as today’s claims data demonstrates: official figures reveal a record monthly rise of 857,000 new benefit claimants. The upsurge takes total benefit claims from 1.24 million to 2.1 million (six times higher than the previous largest monthly rise of 143,000, recorded in February 2009, in the immediate aftermath of the financial crisis). Disconcertingly, the data only partially captures the first full month of lockdown. The cataclysmic economic impact of Covid-19 threatens a repeat of that straitened period.

Elucidating on his opinion, Mr Haldane conveyed the point via simple but alarming addition: 1.3 million claiming out of work benefits prior to the coronavirus outbreak, a further 2 million now unemployed resultant of the crisis, approximately 8 million furloughed under the Government’s job retention scheme, a percentage of which will not return to the workforce as a consequence of economic contraction. Potentially, a further 8 million people working on a reduced or restricted basis. “Add all that and you’ve got anywhere between a third and half the workforce unemployed, under-employed of working fewer hours, many of whom may suffer (a perfectly logical) fearfulness about the reliability of future income and their jobs”. It is worth noting, this disquieting logic excludes the job destruction and business failures among the self employed, of whom there are approximately 5 million.

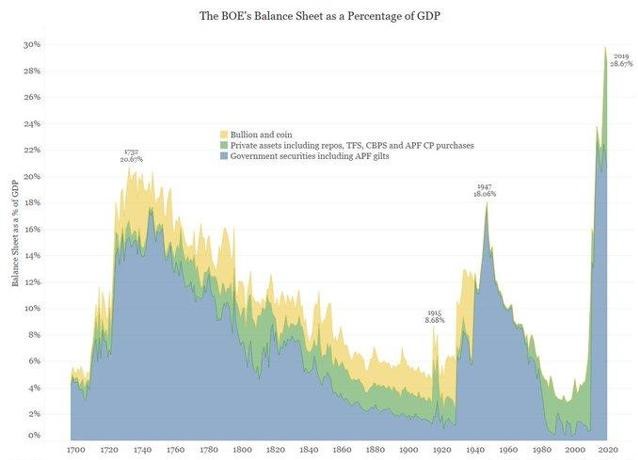

In response to the unprecedented crisis, the Bank of England has embarked on £200 billion of Quantitative Easing and reduced rates to virtually zero (0.1%), in addition to a range of initiatives to support personal and SME lending. The programme of ‘temporary’ QE has now lasted more than a decade at a running total to date of £645 billion.

Bank of England Governor Andrew Bailey, has pledged to do “whatever is necessary”, a now common central bank rejoinder, fuelling heightened market expectations of a further expansion of QE in June, accompanied by intensified speculation about rates crossing the zero bound. On the question of negative interest rates, Haldane is circumspect, but tellingly refuses to rule out adopting the controversial policy. “The economy is weaker than a year ago and we are now at the effective lower bound, so in that sense it’s something we’ll need to look at – are looking at – with somewhat greater immediacy. How could we not be?”

Contemporaneously, Robert Chote, Chairman of the Office for Budget Responsibility, announced a volte-face on previous predictions of a ‘V shaped’ recovery. The economy is likely to see a “slower recovery” from coronavirus than initially anticipated. That particular element of Chote’s remarks a strong contender for ‘understatement of the year‘. Having forecast UK GDP would drop by 35% before returning to similar levels seen before the outbreak in 2021, the OBR now recognise their forecast recovery path to have been excessively optimistic. Mr Chote said the economic challenges posed by the virus would “certainly” lead to higher borrowing, and warned of the “scarring” effect on the economy.

It is now startlingly clear the economic impact of Covid-19 is calamitous, though the precise extent of destruction is incalculable at this juncture, as the duration of the pandemic and and concomitant lockdown remain indeterminate.

While initial attempts at easing restrictions are underway, the process is understandably tentative and incremental, the journey toward a kind of normality assuredly circuitous and prolonged in the absence of a vaccine.

That the Bank of England are very publicly contemplating a policy of negative base rates intimates a PR exercise is underway, via which they are attempting to acclimatise the markets to the prospect of a negative interest rate environment. Such a singular step suggests to this observer previously unknown levels of consternation in regards Britain’s economic stability.

Should these ruminations be realised, as seems probable, the Old Lady of Threadneedle Street will be stepping ‘through the looking glass‘ into a world of extraordinary unconventional monetary policy and in so doing, joining a club of which no Central Banker wishes to be a member.

Both the reality and psychology of adopting a negative interest rate policy are inimical to confidence. Though intended to encourage consumption and augment growth, it is in fact an admission of failure in conventional monetary policy. A decade of historically accommodative base rates in conjunction with £645 billion of Quantative Easing has saturated society in borrowing. If dear reader, you will excuse the emotive analogy, the confidently proffered panacea for 2008 financial crisis maladies has lead the patient to a 2020 economic ICU.

It is recognised that negative rates can cause complications for the banking sector, the very conduit through which central banks wish monetary velocity to be enhanced. The adoption of a policy known to risk antithetical outcomes indicates a level of desperation among the world’s major central banks, which when widely recognised could further undermine already fragile business and consumer confidence.

In March 2020 the Bank for International Settlements (BIS) published a report explaining how negative interest rates can be disadvantageous to banks: ‘If negative policy rates are transmitted to lending rates for firms and households, then there will be knock-on effects on bank profitability unless negative rates are also imposed on deposits, raising questions as to the stability of the retail deposit base. In either case, the viability of banks’ business model as financial intermediaries may be brought into question’.

To provide context, it is important for the unititiated to gain some insight into how banking operates. The business of banking is to borrow relatively short-term and lend longer-term, a process known as ‘maturity transformation‘. Banks take deposits or issue bonds to fund both short-term and long-term lending, from trade finance and business finance for large international corporations and SMEs to individual personal loans. This is called credit intermediation. In practice, banks lend in advance of funding, then fund the drawdown of the loan by borrowing.

Banks earn income on the spread between the interest rates they pay on their borrowing (funding) and the interest rates they receive on their lending. The spread is determined by the risk inherent in specific lending: generally, the riskier the borrower and the longer the tenor of the loan, the higher the interest rate.

It should theoretically be possible for banks to be profitable when rates are very low or even negative. For example, imagine that prior to 2008, a bank paid 5% interest on a 7-day notice deposit account and provided 3-month trade finance at 8%. It would earn a net interest margin of 3%. Now, suppose the benchmark funding rate (e.g. Euribor) has fallen to -0.5%. The bank could pay 0% on its 7-day notice deposit account and provide 3-month trade finance at 3%. Its net interest margin of 3% would remain intact.

However, the BIS says that banks are reluctant to pass on negative rates to smaller depositors. When rates on deposits decline too far below zero, people desist in putting money into bank deposit accounts and resort to using physical cash (notes and coins). This creates funding strain for banks and increases risk and inefficiency in payments.

When interest rates are negative, therefore, banks can struggle with diminishing spreads. Depositors still receive positive interest rates, but the bank is expected to extend business, trade and personal lending at ever lower rates. If banks were to maintain higher rates on lending to preserve their margins, they would defeat the purpose of central bank negative policy rates.

A partial solution to this margin squeeze might be for banks to pursue riskier lending, by for example, providing more business finance to SMEs, or more highly geared personal lending. However this type of lending is capital intensive and current economic turmoil is not conducive to enhanced risk appetite.

Since the 2008 financial crisis, banks have been under regulatory pressure to build up capital and liquidity buffers to protect against bank runs and loan defaults. Owing to the way risk weightings work for the purpose of capital allocation, riskier lending requires more capital than forms of lending regarded as safer, (e.g. residential mortgages). The BIS reports that banks have built up their capital buffers principally by retaining earnings, though reducing risky assets on their balance sheets and issuing more equity have also been important.

Negative rates can potentially produce unintended deleterious outcomes in two ways:

1. Declining share prices suggest that investors don’t believe banks can be consistently profitable in a low-rate, low-growth environment, so become reluctant to invest. As share prices deteriorate, it becomes more difficult for banks to raise the capital they need to support riskier lending.

2. Bank profitability decreases, it becomes harder for banks to build up capital by retaining earnings. Increasing risky lending becomes unachievable when profitability is constrained and capital expensive.

Paradoxically then, breaching the zero bound and implementing a negative interest rate policy can produce outcomes obverse to those sought, while intensifying unfavourable conditions for a banking system already bracing itself for a tsunami of defaults.

We are now facing the fourth significant economic crisis of the millennium, each in turn palliated not cured, with an ever greater expansion in credit, abetted by central banks’ unnatural suppression of interest rates and repeated deluges of additional money supply.

Britain, as all Western nations, has gorged at the trough of bottomless credit, becoming distended and dependent. After repeated doubling down, we appear to have reached a vanishing point, where the only remaining option is a distorted inversion of monetary policy.

Given the prevailing apocalyptic presentiment, it is perhaps unsurprising those seeking viable alternative solutions should look to earlier economic concepts for inspiration. One such is the Austrian Business Cycle Theory (ABCT) and its two most prominent proponents, Ludwig von Mises and Freidrich Hayek. According to the former, “there is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as a result of the voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved”.

A profound indictment of twenty first century policy making.

Stephen Cherry. 18th May 2020.