As Covid 19 ravages the economy and the concomitant costs of mitigation continue to spiral, the debt debate is prompting paroxysms of anguish. Opinion is firmly divided, each side becoming more entrenched and more certain of the other’s inefficacy.

Leaked confidential Treasury assessments of the coronavirus crisis estimate a cost to the Treasury of circa £300 billion in 2020. The ‘market sensitive’ document reveals a ‘base case scenario’ where Britain will face a budget deficit of £337 billion this year, compared to the £55 billion forecast at the Budget.

Even in the more ‘optimistic scenario’ of a ‘V shaped’ recovery, where economic output falls sharply but recovers with equal rapidity, the deficit is still forecast to be in the region of £210 billion this year.

In the ‘worst case scenario’, an ‘L shaped’ economic decline, where output falls sharply and reduced output persists, the deficit figure increases to an eye watering £516 billion in the current financial year, rising to a cumulative £1.19 trillion over a five year forecast.

With the global economy rendered moribund by government dictum for an indeterminate and potentially prolonged period, inflicting immediate unprecedented financial damage and incalculable longer-term destruction of the economic base, the ‘L shaped’ scenario appears disconcertingly plausible.

Such portentous economic predictions provide stark context to the conflicting choices, perhaps informing the timing of the Government encouraging people to return to work.

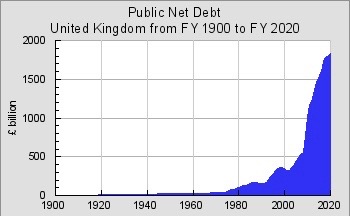

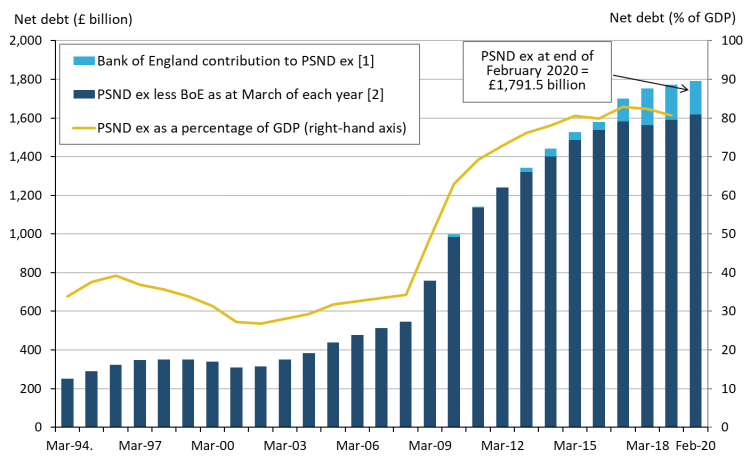

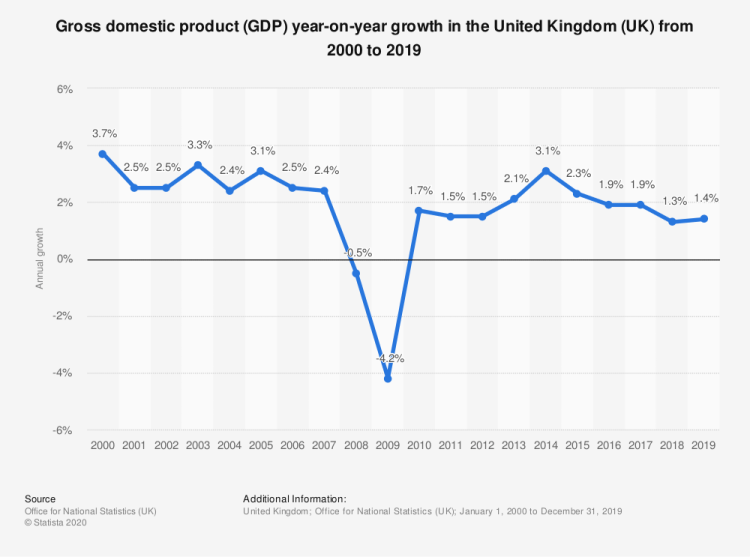

UK Public Sector debt stood at £1,791.5 billion at the inception of the current crisis. Under the ‘L shaped’ scenario, PSND potentially exceeds £3 trillion over the five year time horizon to 2025. In the years after the 2008 financial crisis, the UK debt to GDP ratio expanded by a factor of three, toward 90%. The pessimistic Treasury prediction implies a significant rise toward 130% (assuming GDP as a constant). When considering UK Gross Domestic Product declined 4.2% between 2008 and 2010, and estimates for 2020 GDP average -14%, calculations based upon undiminished GDP during this period of unparalleled global economic disruption, require courageously positive presumptions.

Treasury officials have advised Chancellor Rishi Sunak that ‘stabilising the debt dynamics’ could involve raising £80 billion to £90 billion a year through a combination of tax rises and spending reductions. According to the documents, the Chancellor ‘has indicated a preference for a higher but broadly stable level of debt’. However, it notes ‘as debt is likely to reach significantly higher levels after the crisis, it will be important to stabilise the debt-to-GDP ratio and prevent debt from continuing to grow on an unsustainable trajectory’.

The ‘Treasury View’ however, has caused consternation among commentators who hold the antithetical opinion, believing that additional borrowing (at current historically low interest rates) to support the economy during the pandemic driven contraction is essential. Economist Olivier Blanchard is oft cited in support of this position: “A situation in which interest rates are expected to remain below growth rates for a long time, is more historical norm than exception. If the future is like the past, the issuance of debt without a later increase in taxes, may well be feasible. Put bluntly, public debt may have no fiscal cost”.

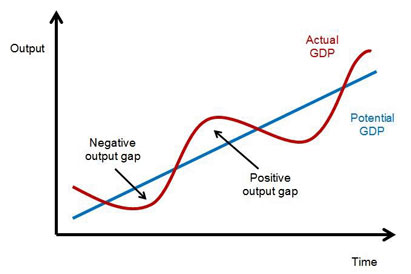

A further pillar of support for this perspective is the ‘Output Gap’ assertion. According to its advocates, when an economy displays material slack, or a significant output gap, the fiscal multiplier of public investment and infrastructure is extremely high. The borrowing pays for itself by boosting GDP, lowering the debt ratio over time (ceteris paribus).

Given the sheer magnitude of risk inherent in pursuing a mistaken fiscal policy, it is worth interrogating each of these contentions in turn:

If, as so often, the future proves to be unlike the past, if even historically low interest rates are higher than growth, owing to sustained negative GDP, persistent issuance of public debt can produce significant fiscal costs, in deleterious combination with a ‘crowding out’ of private investment, which would be detrimental to future growth.

As Harvard economist Kenneth Rogoff posited late last year, ‘complacency regarding much higher debt implicitly assumes the next crisis will look just like the last one in 2008, when interest rates on government debt collapsed. But history suggests that this is a dangerous assumption. The next wave of crises could require governments to simultaneously stall the capitalist engine and spend vast sums on remediation with unknown ramifications for growth and interest rates’. Prophetic words indeed.

Highlighting another aspect of risk in large scale escalation of debt issuance, Nobel laureate economist Robert Lucas’s critique observes ‘big shifts in policy can backfire owing to comparable shifts in expectation. Aggressive experimentation with much higher debt might cause a corresponding shift in market sentiment’ leading to a consequential rise in borrowing costs.

The ‘Output Gap’ assertion can only hold true when actual GDP growth is negative to potential GDP (the material slack). A probable consequence of the pandemic shutdown, owing to destruction of the economic base, through rising unemployment, corporate contraction or closure and the consequent cascading effect of loan defaults, is a diminution of potential output, leading to a resultant ‘positive’ output gap – where even suppressed ‘recessionary’ output exceeds the damaged level of potential.

The anomalous nature of the Covid crisis and the consequent collapse in tax receipts, has necessitated prodigious debt issuance, simply to finance monumental remediation expenditure. These public disbursements constitute Government’s attempt to hold the economy in suspended animation for the duration of lockdown, they do not however, represent any form of infrastructure expenditure. Nor is a significant fiscal multiplier assured. (Mutatis mutandis).

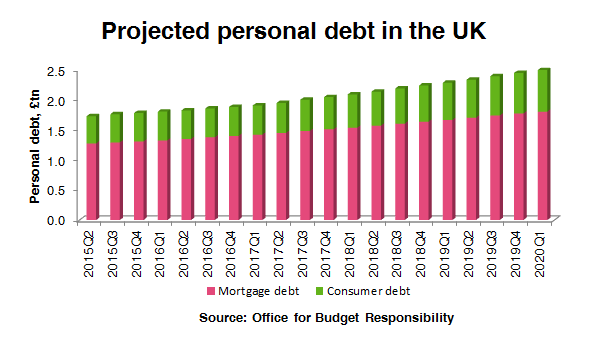

Simultaneous to the rise in UK public debt has been the explosion in personal indebtedness. Extraordinarily, personal borrowing in Britain stands in equivalence to the national debt, at approximately $1,700 billion. Some 75% of the this figure is mortgage borrowing, the remainder representing personal loans, credit card balances, vehicle PCPs etc.

As property prices ascended, particularly in the immediate aftermath of the Bank of England QE programme, loan to values climbed exponentially, while changes in income were, until very recently minimal to negative on an inflation adjusted basis. This meant many buyers committed to borrowing ever larger multiples of income, often with minimal deposits. Now unemployment threatens to undergo a dramatic rise and lenders have withdrawn many competitive mortgage structures, a market of often low equity and loaded borrowing appears very fragile.

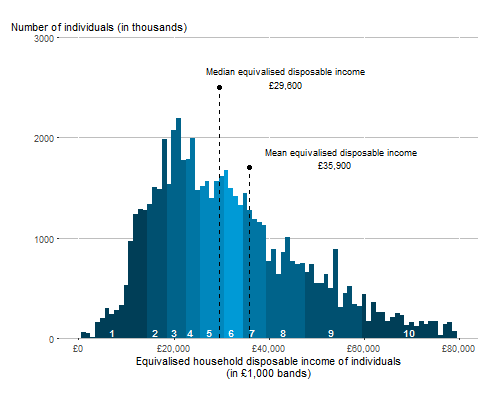

Another thread of borrowing worth pulling on is Personal Contract Purchase (PCP). These deals have proved immensely popular over the last decade, ostensibly owing to the fact they require a minimal deposit and offer manageable monthly payments. This alchemical combination is based on the notion of a ‘Future Guaranteed Value’ (FGV) for the vehicle in question. This can be represented by the simple equation (deposit plus 36 monthly payments plus FGV equals zero). Median annual income is £29,600 and the average new car price is £33,559, total sales in excess of 2 million per-annum are thus rendered explicable: the majority of passenger cars in Britain are in essence long-term rentals. Drive for three years, return the keys and repeat. However, economic uncertainty is beginning to unravel these highly prevalent structures from both ends: the ‘manageability’ of payments is becoming doubtful as employment prospects deteriorate, prompting fears of en masse defaults, while the fundamental FGV is being undermined as car sales collapse around the globe, leaving manufacturer finance companies with multiple ‘value’ shortfalls.

Battle rages on both health and economic fronts simultaneously, the depth of economic damage being wrought across the nation only just becoming clear. Records of an unwanted nature are likely to be set across every sector of the economy, every section of society adversely effected. Cascading failure across personal and corporate debt may now be unavoidable, economic contraction and surging unemployment inescapable.

As the national debt inevitably climbs, the government must consider with the utmost care, the attitude it will adopt and timescale to which it will adhere in relation to sovereign borrowing. While Britain is better placed than many of its EU neighbours, owing to the parlous position of the Eurozone (dysfunctional structures, member states no longer able to borrow in a currency over which they have monetary control, a trammelled central bank, judicial imbroglio, constitutional crises, debt crises culminating in an existential crisis) and our superior constitutional settlement – independent central bank, national currency, global financial centre etc, the nation’s continued ability to tap bond markets, our international standing and future prosperity in a post-Brexit world are all at stake. (Qui mutuum accipit cave).

Stephen Cherry. 15th May 2020.