Bank Publishes Deeply Despondent Economic Forecast for 2020. Optimistic Predictions For Recovery Are Made Through A Glass Darkly

The UK economy will contract by 25% in the Second Quarter 2020 the Bank of England cautioned today, before staging a recovery “relatively rapidly” through the second half of the year, assuming lock down restrictions are significantly eased.

This equates to a decline in GDP of 14% year-on-year. A recovery of 15% in 2021 is optimistically conjectured, predicated on a central expectation of the economy returning to a sustainable form of normality.

Bank officials predict a rise in unemployment to 9% from the current 4%, followed by a gradual improvement toward pre-pandemic levels by 2022. Disquietingly, these figures exclude the 6.3 million workers furloughed under the government’s job retention scheme.

Governor Bailey declared “we expect the effects on demand in the economy will go on for about a year after the lockdown starts to lift. We also expect there will be some longer-term damage to economic capacity, but in this scenario we judge these effects to be relatively small”.

By necessity, the Governor introduced caveats to the Bank’s central forecast: “The timing of the recovery will depend in large part on how long both social distancing and support measures are in place. The speed of recovery will also be affected by how households and businesses respond once measures are lifted”.

Given the multitudinous imponderables of the crisis and numerous, potentially life-threatening pitfalls of misjudging even marginal changes to government policy, the Bank’s more pessimistic (tail risk) assumptions bear closer scrutiny.

The economic fallout will be more deleterious should restrictions remain in place longer than expected. Continuation of lockdown and support measures costs an additional 1.25% of GDP. Extra precautionary saving by households could depress GDP by 1% while permanently elevated unemployment could subtract a further 1%. Surprisingly, the Bank’s central (optimistic) scenario takes no account of a potential second wave of coronavirus infections during Autumn/Winter 2020/21.

The Bank’s financial stability report warns that its central forecast scenario would leave companies with a £140 billion cash deficit caused by the lockdown. Adding, some businesses will need access to additional sources of finance to maintain their productive capacity through the period of economic shock.

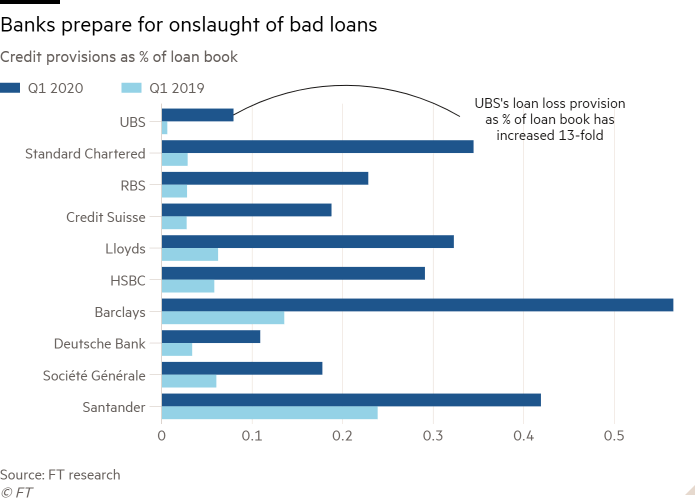

In the aftermath of the 2008 Financial Crisis, Britain’s banks were subjected to years of stress tests to ensure their ability to survive a serious recession. The depth and rapidity of this crash exceeds the hypothetical stresses envisaged by that process. Banks are forecast to see their financial buffers halved by the recession, a reduction caused by £80 billion of credit losses, incurred in UK and overseas lending, defaults in corporate credit, consumer credit and mortgages.

Bank of England officials expect the banking system to remain sufficiently stable to continue lending, an assumption based in large part on the job retention scheme protecting millions of jobs and a concomitant sharp recovery.

Bank officials left open the possibility of further monetary easing, in the shape of an additional £100 billion in quantitative easing, declaring themselves “vigilant to risks emerging”. Only two of the nine Monetary Policy Committee (MPC) members voted to expand QE from £200 billion to £300 billion, but economists have divined this as a sign of easing in the near term.

At 7pm on Sunday 10th May, Prime Minister Boris Johnson will lay out his step-by-step strategy for phase two, ‘the roadmap’ out of lockdown. Many will be hoping for a decisive change in direction, heralding a return to a version of normality, while others will be uncertain of the wisdom in policy moderation. Proceeding with ‘maximum caution’ is a phrase attributed to Downing Street in the press, and in this writer’s opinion for good reason. The government faces a Morton’s Fork of epic proportions: to delay an easing of restrictions is to inflict yet deeper economic damage, to miscalculate the timing and focus of such changes could be lethal.

Political necessity obliges at least a reinterpretation of the restrictions, but given the inherent risk, disappointment at the paucity of change is likely to be the nationwide reaction.

In this context, the Bank of England’s central forecast scenario of what can be essentially described as a V shaped recovery appears overtly optimistic. The Bank must obviously chart a calm and moderate course through these dangerous and truly uncharted waters, offering ameliorating opinion whenever possible. However, as posited in previous pages, the scale of destruction to productive capacity, fiscal, socioeconomic and health outcomes this crisis could potentially inflict are incalculable. Perhaps BoE and Treasury officials alike, surmise that publishing estimates of extreme economic devastation is simply counterproductive.

Stephen Cherry. 7th May 2020.